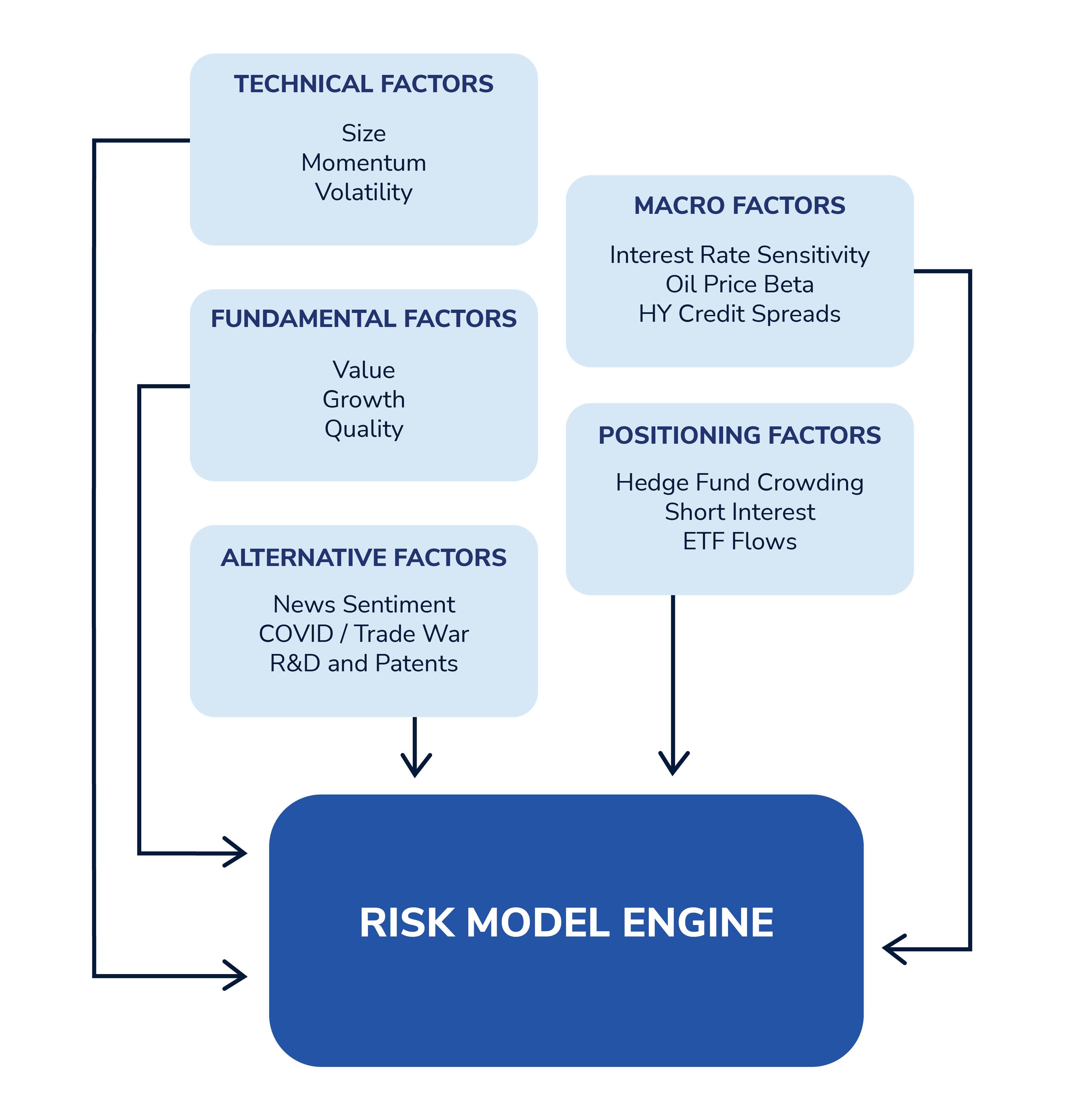

Risk Models | Our risk model engine leverages our 300+ risk factor library and cloud-based platform to quickly generate multi-factor equity risk models with coverage of 45,000+ global securities. Our next generation factors like hedge fund crowding and interest rates are not found in conventional models. We offer a suite of off-the-shelf models as well as custom models tailored to investment mandates or current market dynamics. We deliver flatfiles directly to clients pre-market, send risk models to third-party platforms, and offer access to our risk model API.

Attribution | Our state-of-the-art portfolio attribution system is designed to meet the needs of fundamental discretionary PMs who find conventional attribution analysis lacks intuitive value, systematic managers who want to leverage some of our proprietary techniques, and CIOs/CROs who want to make more informed manager allocation and hedging decisions. We offer portfolio attribution as a managed service, our Factor Awareness Dashboard to conduct ad-hoc analysis, and partnerships with third-party attribution platforms.

Hedge Solutions | Our in-house QES optimizer, attribution system, and risk model engine are seamlessly integrated to provide tradable risk solutions. Style factor hedges are precise and affordable with embedded leverage to the target factor. Smart beta hedges are customized to your portfolio to be more effective at offsetting systematic risks than off-the-shelf ETFs/futures. Portfolio tilts suggest small weight adjustments that maintain consistency between position-sizing and PM conviction on alphas while mitigating an undesired factor exposure.

Research | The QES team publishes market-relevant signals to quantify new risks as they emerge, and these can be quickly incorporated into our risk models and tradable solutions. Our style, country, and industry rotation models and factor crowding models are also highly relevant for risk managers. We also publish technical papers on innovations in risk model design, attribution techniques, and portfolio construction. Risk Solutions clients have access to the broader QES research publications, conferences, and team members.

Research Consulting | The QES Risk Solutions team offers risk consulting services to clients on an ad-hoc or ongoing basis. We leverage our in-house research & tools as well as our expertise in risk models, portfolio construction, and tradable products to advise clients on portfolio risks and solutions. We work directly with portfolio managers, traders, risk teams, and the C-suite across a wide range of investment mandates.

Our team has standard fundamental risk models in the following categories…

Our Team

The QES Risk Solutions effort was launched after the successful work of Luo’s QES team to innovate in equity risk management to improve their own alpha strategies. The Risk Solutions team sources the broader QES team’s deep expertise in signal construction via their factor library to power its proprietary risk model engine, attribution library, portfolio optimizer, and hedge frameworks. The Risk Solutions team includes experts in risk management, equity markets, portfolio construction, quantitative research, technology, and product development. The team strives to engage not only risk managers but to support investment decision-makers including PMs, traders, and CIOs with relevant insights and actionable solutions. We work directly with institutional clients, providing products and tools as well as consulting services. We also partner with top-ranked broker-dealers and fintech firms so our IP is fully integrated with third-party platforms that offer attribution UIs, decision-support analytics, and execution capabilities.

Our Partners

Omega Point offers an intuitive, turnkey platform that quant-enables investment teams to adapt to today’s data-rich, factor-driven markets with seamless control and precision. Leading asset managers, hedge funds, banks, and other financial institutions rely on Omega Point’s portfolio intelligence tools and services, and single-point access to the industry’s first open, integrated ecosystem of information services providers, technology partners, and brokers. Partnered with Wolfe Research since 2019, Omega Point offers its users turnkey access to Wolfe QES risk models, including: US Broad Risk Model, Developed Markets Risk Model, individual Sector Models, and others.

Visit Omega Point

EDS offers Investment Process Management solutions through a fully configurable, scalable platform to support investment decision-making — from idea generation, research management (RMS), portfolio construction to risk management and performance attribution analytics. Leading fundamental investors including hedge funds and asset managers rely on EDS to digitally transform their workflows and centralize their intelligence, proprietary and third-party, for a single source of truth. EDS seamlessly integrates Wolfe QES risk models and factors with a host of other data sources to deliver a cost-effective, flexible platform for an optimized investment process, higher performance and productivity, and making more informed decisions.

Visit EDS

Goldman Sachs and Wolfe Research are combining their risk expertise and factor data to power your investment decision-making workflow. This integration is made available to institutional investors through Goldman Sachs Marquee, with Wolfe’s factor models available programmatically or via Marquee’s intuitive web interface.

Visit Goldman Sachs Marquee

In Instinet Analytics | TradeSpex Strategy, you can find a suite of single-stock and portfolio pre-trade analytics that uniquely integrate trading, portfolio construction, management and risk analytics to deliver a complete workbench solution. These robust visualization and analysis tools provide clarity and confidence before every trade.

Visit InstinetWhat Differentiates Our Products?

Next Generation Style Factors – Our models include conventional technical and fundamental factors plus next generation factors that improve explanatory power and are intuitive to investors.

Enhanced Stock Exposures to Factors – Instead of relying solely on cross-sectional rankings of stocks based on a particular signal, we incorporate the stock’s statistical sensitivity to each factor. This reduces ex-post correlations between alpha and factors resulting in more effective risk management.

Expanded Model Coverage – Each of our risk models covers 45,000+ stocks globally, so equity positions outside of the model’s target investment segment can be modeled without losing explanatory power by moving to a broader model.

Holdings-Based Factor Covariances – We predict correlations based on today’s factor portfolios instead of using historical compositions. This makes our factor covariance matrix more responsive to signal turnover

Alignment of Factor Portfolios and Returns – Some vendors re-estimate FMP compositions after the market close to remove extreme stock returns then report FMP returns based on the updated portfolios. We report FMP returns for the portfolios delivered before the market opens.

Intelligent Residual Risk – Conventional vendors use the inverse of the square root of market-cap as a proxy for idiosyncratic risk. Our approach uses a separate multi-factor model to more accurately estimate the idiosyncratic risk for each stock.

QES Risk Products test

Click on the symbol to view our products:

![]() Tear Sheet (must be an institutional investor to view)

Tear Sheet (must be an institutional investor to view) ![]() White Paper (must be a client to view)

White Paper (must be a client to view)

Risk Models

Attribution

| Name | Description | |

|---|---|---|

| Attribution API (Beta) | Our attribution API provides the same proprietary tools used by Wolfe's QES team directly to our clients in a programmatic interface. Users can leverage productionized risk models or connect to our risk model API to use on-the-fly models to run portfolio attributions. Our API is fast and fully flexible to provide timeseries analysis and security-level details for global portfolios. | |

| Attribution Service | We provide portfolio attribution service directly to clients using off-the-shelf or custom risk models. Clients provide portfolio holdings, and we provide automated attribution reports on a daily or monthly basis. Attribution reports include timeseries analysis, security-level details, and PM/strategy breakdowns. Standard templates are provided in Excel and PDF format, and machine readable attribution data is also available. Reporting can also be customized for client needs. | |

| EDS | EDS provides attribution functionality and can integrate both factor libraries and risk models from the Wolfe QES team through our partnership. This Investment Process Management solution is a fully configurable, scalable platform to support investment decision-making - from idea generation, research management, portfolio construction to risk management and performance attribution analytics. | |

| Factor Awareness | The Portfolio Attribution tab on our flagship website allows clients to run ad-hoc attributions for live portfolios uploaded by the user with any risk model from standard suite. Users can easily view the sources of risk and recent returns in a portfolio or stock, evaluate their portfolio relative to a benchmark, see the impact of ETF overlays, and import Wolfe custom baskets. Clients can also view and download historical factor returns from our risk models. | |

| GS Marquee | GS Marquee provides portfolio attribution and basket construction functionality that leverage Wolfe QES risk models through our partnership. | |

| Omega Point | Omega Point provides portfolio intelligence tools powered by Wolfe QES risk models and factor libraries through our partnership. Omega Point offers on an intuitive, turnkey platform that provides portfolio intelligence tools and services to quant enable investment teams to adapt to today's data-rich, factor-driven markets with seamless control and precision. |

Tradeable Solutions

| Name | Description | |

|---|---|---|

| Optimizer API (Beta) | Our optimizer API provides the same proprietary tools used by Wolfe's QES team directly to our clients in a programmatic interface. The optimizer API integrates alpha signals, risk models, and operational constraints into tradable portfolios and provides access to our library of proprietary hedge frameworks. | |

| Portfolio Tilts | Portfolio tilts suggests small shifts in weights across the portfolio to mitigate an undesirable factor exposure without significantly altering the rank order of conviction implicit in position sizing. This solution is most relevant for long-only managers or those who can't use derivatives or ETF overlays to mitigate undesirable risks. | |

| Smart Beta Hedges | Our proprietary smart beta hedges offer more precise and effective solutions for mitigating systematic risks to isolate stock-specific alpha than off-the-shelf beta hedges. These short-only (or long-only) tradable solutions can be applied to portfolios or single-stocks, leveraging both Wolfe's innovations in both risk model design and hedge construction. We monitor live hedges post-trade to ensure ongoing alignment with the hedge objectives. Clients can trade custom hedges on swap with our broker-dealer partners. | |

| Factor Hedges | We leverage our expertise in portfolio construction and risk management to deliver precise and affordable style factor hedges. These long-short hedges are designed to target one or more factors from a risk model. We use proprietary techniques to amplify the target exposures and reduce the required hedge ratios without taking on significant idiosyncratic risk or exposures to non-targeted factors. We monitor live hedges post-trade to ensure ongoing alignment with the hedge objectives. . Clients can trade custom hedges on swap with our broker-dealer partners. | |

| Wolfe | Nomura Baskets | These off-the-shelf solutions provide factor, sector, macro, and thematic exposures in tradable format leveraging the Wolfe QES factor library and expertise in signal construction. These baskets are designed to provide highly liquid, systematic exposures with minimal idiosyncratic risk. New baskets are launched on an ongoing basis to address topical risks in the current market environment. |